You will need to understand the following terms/definitions. Take a few moments to familiarize yourself with them and commit them to memory; you will encounter them in this lesson. You will have a chance to test your memory during the Terminology Game and the Crossword Puzzle.

Allocate

To assign an item of cost, or a group of items of cost, to one or more cost objectives. This term includes both direct assignments of cost and the reassignment of a share from an indirect cost pool.

Direct Cost

Any cost, which is identified specifically with a particular final cost objective. Direct costs are not limited to items which are incorporated in the end product as material or labor. Costs identified specifically with a contract are direct costs of that contract. All costs identified with other final cost objectives of the contractor are direct costs of those cost objectives.

Indirect Cost

Any cost not directly identified with a single final cost objective, but identified with two or more final cost objectives or with at least one intermediate cost objective.

Indirect Cost Pool

A grouping of incurred costs identified with two or more objectives but not identified specifically with any final cost objective.

Previously you learned how to navigate to the e-CFR website, the source to refer to for the current Cost Accounting Standards. You can go to it anytime you wish. Refer to the job aid under Lesson Resources if you need a refresher on how to access it.

For the purposes of this course however, we have provided an annotated version of CAS 418, to assist you in navigating the CAS and to help you focus on the key take away points in each standard. After reading the highlighted portions of the CAS, the lesson will walk you through several exercises to reinforce your learning.

Select the icon to read the annotated version of CAS 418.

After you have finished reading, we’ll review key points throughout

the rest of the topic.

Video T&D

Professor Oliver is standing next to his whiteboard. CAS 418 is written at the top of the whiteboard in bold type, as Oliver begins: "CAS 418 has three major purposes, all related to direct and indirect cost allocations." As Oliver says: "First, it provides for consistent determination of direct and indirect costs," Number 1 is written on the whiteboard, followed by: Consistent determination of direct and indirect costs. As Oliver says: "Second, CAS 418 provides criteria for accumulating indirect costs into indirect cost pools," Number 2 is written on the whiteboard, followed by: Criteria for indirect cost pool. As Oliver says: "And third, CAS 418 provides guidance related to selecting allocation measures based on the beneficial or causal relationship between an indirect cost pool and cost objectives," the Number 3 is written on the whiteboard, followed by: Allocation measures.

As Oliver goes on to say, "Let's begin by distinguishing between direct costs and indirect costs, since this is fundamental to this topic," those two words are added to the whiteboard in large, bold type: Direct Costs and Indirect Costs.

At this point, Indirect Costs partially fades out on the whiteboard to place the focus on Direct Costs as Oliver goes on to say: "A direct cost is any cost which is identified with a single, final cost objective." Arrows representing direct costs flow to a contract for the next generation surveillance drone that spirals into view, as Oliver continues: "For example, a contractor is awarded a contract to design the next generation surveillance drone. This is one of five contracts in the business unit. The labor costs of those who work directly on the drone contract, such as the engineers, and the costs of the parts for the drone are direct costs of the contract." As Oliver is explaining this, the label Engineers is added to the first direct cost arrow and the label Parts is added to the second direct cost arrow. Oliver goes on to say: "These labor and material costs are charged directly to the drone contract. In the next presentation, I'll explain indirect costs."

Video T&D

Professor Oliver is standing next to his whiteboard. CAS 418 is written at the top of the whiteboard in bold type, as Oliver begins: "Now that you know what direct costs are, let's focus on indirect costs, including what they are and how they are allocated to final cost objectives." The words Indirect Costs are added beneath CAS 418 on the whiteboard, as Oliver continues: "Indirect costs are those costs that cannot be identified directly with one final cost objective and that apply to two or more final cost objectives."

At this point, a swimming pool slides into view that is labeled Labor Overhead Pool as Oliver says: "Continuing with the next generation surveillance drone example, there are some managers, supervisors, and others who support all five of the contractor's contracts and whose costs cannot be allocated directly to any of the contracts." As Oliver is speaking, five contracts appear above the pool.

As Oliver says: "Therefore, these costs are pooled together in the Labor Overhead Pool. The total labor overhead pool is $4,000,000," the amount $4,000,000 appears in the pool. Oliver asks: "How do we allocate the $4,000,000 labor overhead costs to each of the five contracts?" As Oliver says: "We need to use an allocation base that will result in each contract receiving its fair share of the overhead costs," five arrows appear in the pool extended from the $4,000,000 in the pool to each of the five contracts above the pool. Oliver continues, "In this case, we'll use direct labor dollars as the allocation base."

The heading CAS 418 and subheading Indirect Costs remain on the whiteboard; everything else disappears as Oliver says: "Total direct labor costs for the accounting period amounted to $40,000,000. $4,000,000 labor overhead divided by $40,000,000 in direct labor dollars equals a labor overhead rate of 10%." As Oliver is explaining, the following equation is written on the whiteboard, and then 10% Labor Overhead Rate is highlighted for emphasis. Equation: $4,000,000 Labor Overhead / $40,000,000 Total Direct Labor Costs x 100 = 10% Labor Overhead Rate.

Oliver goes on to say: "To calculate each contract's fair share of labor overhead, we'll apply the 10% overhead rate to the direct labor dollars of each contract."

Everything on the whiteboard is erased except the heading CAS 418 and subheading Indirect Costs, and then the drone contract spirals back into view as Oliver continues: "For the drone contract, if the total direct labor dollars amounted to $12,000,000, what is the fair share of labor overhead for that contract?" As Oliver is asking this, $12,000,000 Direct Labor Dollars is written on the whiteboard beside the drone contract.

Oliver concludes by saying: "If you said it would be $1,200,000 by taking 10% of $12,000,000, you earned the gold star," as this equation is added to the whiteboard: $12,000,000 x 10% = $1,200,000 Labor Overhead Indirect Cost.

Now that you know the major purposes of CAS 418, let’s go over the most important requirements of CAS 418.

Select each for more information.

One major requirement is that CAS 418 requires that business units have a written policy for how they classify costs as direct or indirect. This policy will be included in their Disclosure Statement—a written description of the contractor’s cost accounting practices and procedures.

Another major requirement of CAS 418 is that contractors’ indirect cost pools must be homogeneous. If each significant activity within the cost pool has the same or similar beneficial or causal relationship to the cost objectives as the other activities in the pool, then the pool is homogeneous. In this topic, you’ll learn how to determine if an indirect cost pool is homogeneous.

CAS 418 gives specific criteria to aid in selecting a proper allocation base. If there are significant costs of management or supervision in the pool, then the contractor must use an allocation base that is representative of the activity being managed or supervised.

If there are no significant management or supervision costs, the indirect cost pool must be allocated over a base that is representative of resource consumption, using either a resource consumption measure, an output measure, or a surrogate that is representative of the resources consumed.

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

A contractor has a written policy stating that direct and indirect costs are classified on a case-by-case basis at the discretion of the Chief Financial Officer.

CAS 418 includes requirements related to standard costs. Before we examine those requirements, we need to explain what standard costs are and why they are sometimes used.

Select each question below for important information.

The use of standards was more prevalent in the past, prior to the widespread use of enterprise resource planning (ERP) software. ERP software monitors and reports performance data, along with a lot of other useful data, nearly in real time.

Some defense contractors continue to use standards as management tools to establish benchmarks to measure performance. On a regular basis, they compare the actual costs to the standard costs. If there are material variances between the standard and the actual costs, this signals that the standard isn’t being met, and there may be a problem.

A standard cost is any cost computed using a pre-established standard, such as the amount of time the activity should take and/or how much it should cost. A standard could be an estimate of time or an estimate of money, such as estimated unit cost.

As a common example, traditionally what is the standard time for an oil change? If you said 30 minutes, you’re right! When estimating costs of oil changes, the standard of 30 minutes is typically used.

CAS 407

CAS 418 specifies that when accounting for direct costs, the business unit may use standard costs for direct material or direct labor as long as the requirements in CAS 407 are followed.

“In accounting for direct costs, the business unit must use actual costs, except that standard costs for material and labor may be used as provided for in CAS 407.”

[48 CFR 9904.418-50(a)(2)(i)]

CAS 407

CAS 418 specifies that when accounting for direct costs, the business unit may use standard costs for direct material or direct labor as long as the requirements in CAS 407 are followed.

“In accounting for direct costs, the business unit must use actual costs, except that standard costs for material and labor may be used as provided for in CAS 407.”

[48 CFR 9904.418-50(a)(2)(i)]

Requirements

CAS 418 says: An average cost or pre-established rate for labor may be used provided that:

(A) The functions performed are not materially disparate and employees involved are interchangeable with respect to the functions performed, or

(B) The functions performed are materially disparate but the employees involved either all work in a single production unit yielding homogeneous outputs, or perform their respective functions as an integral team.

[48 CFR 9904.418-50(2)(ii)]

Example 1

A contractor has a pre-established rate for machine maintenance. The functions involve repairing the machines. The maintenance department has 30 employees, and all 30 employees can perform maintenance on all the company machines.

Is the contractor’s use of a pre-established rate, under these circumstances, compliant with CAS 418-50(a)(2)(ii)(A)? What do you think?

Yes, provided the standard costs comply with CAS 407, this practice complies with CAS 418-50(a)(2)(ii)(A) because the functions performed are interchangeable and the employees are interchangeable.

Select the Q/A question when you are ready to check your answer.

Example 2

A contractor proposes using a pre-established rate of $50 an hour for each of its 70 workers. This contractor produces the navigation systems for unmanned aerial vehicles. While there are different types of workers in the department, the end product is always the same—identical navigation systems.

Will the contractor’s use of a pre-established rate comply with CAS 418-50(a)(2)(ii)(B),

in this case?

Yes, this practice complies with CAS 418-50(a)(2)(ii)(B) because the workers are in a single production unit yielding homogeneous outputs.

Select the Q/A question when you are ready to check your answer.

Example 3

A contractor is using a pre-established rate in a department with disparate workers who all work together as an integral team.

Is the contractor’s use of a pre-established rate compliant with CAS 418-50(a)(2)(ii)(B), in this situation?

The answer is yes, the use of a pre-established rate complies with CAS 418-50(a)(2)(ii)(B) because the workers, even though they perform disparate tasks, all work together as an integral team.

Select the Q/A question when you are ready to check your answer.

Variances

When average cost or pre-established rates are used, variances must be disposed of, i.e., corrected, at least once a year. This means the contractor must compare the actual costs to the standard costs and correct any material variances. The specific CAS wording is:

Whenever average cost or pre-established rates for labor are used, the variances, if material, shall be disposed of at least annually by allocation to cost objectives in proportion to the costs previously allocated to these cost objectives.

[48 CFR 9904.418-50(a)(2)(ii)(B)]

Variances

When average cost or pre-established rates are used, variances must be disposed of, i.e., corrected, at least once a year. This means the contractor must compare the actual costs to the standard costs and correct any material variances. The specific CAS wording is:

Whenever average cost or pre-established rates for labor are used, the variances, if material, shall be disposed of at least annually by allocation to cost objectives in proportion to the costs previously allocated to these cost objectives.

[48 CFR 9904.418-50(a)(2)(ii)(B)]

Question

For example, a contractor uses a pre-established labor rate for its collating department. The contractor’s fiscal year ends on December 31. The contractor has a policy of disposing of any material variances on June 30 of each year.

Does this practice comply with CAS 418?

The answer is yes, this practice complies with CAS 418. The contractor must dispose of the variance annually. However, there is no requirement that the variances be disposed of at the end of the fiscal year.

Select the Q/A question when you are ready to check your answer.

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

Recall that Cost Accounting Standard (CAS) 418-50(a)(2)(ii)(A) says that an average cost or pre-established rate for labor may be used provided that the functions performed are not materially disparate and employees involved are interchangeable with respect to the functions performed.

A contractor has a pre-established rate for maintenance work. The maintenance department consists of fifty employees. Twenty of these employees perform maintenance on the company’s fabrication machines while the other thirty perform maintenance on the assembly machines. Due to the unique characteristics of the fabrication and assembly machines, only five of the fifty employees are assigned to work on both fabrication and assembly machines. The functions involve the general upkeep of the machines.

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

Recall that Cost Accounting Standard (CAS) 418-50(a)(2)(ii)(A) says that an average cost or pre-established rate for labor may be used provided that the functions performed are not materially disparate and employees involved are interchangeable with respect to the functions performed.

A contractor has a pre-established rate for machine work. The maintenance department consists of fifty employees. The maintenance department performs both maintenance and overhaul. Maintenance functions involve minor repairs and upkeep that maintain the workability of the machines.

The overhaul function involves machine refurbishment, which requires substantial rework. The overhauls extend the life and/or improve the usefulness of the machines. All of the employees in the maintenance department are capable of performing both maintenance and overhaul work.

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

Recall that Cost Accounting Standard (CAS) CAS 418-50(a)(2)(ii)(B) says that an average cost or pre-established rate for labor may be used if the functions performed are materially disparate but the employees involved either all work in a single production unit yielding homogeneous outputs, or perform their respective functions as an integral team.

A group of workers operate in the Computer Troubleshooting Department, which is responsible for troubleshooting computer problems with company customers. Some of the workers specialize in software debugging, while others specialize in hardware. Sometimes it is not possible to immediately identify whether the problem involves software or hardware, so two workers are assigned to the problem (one that has expertise in software and one that has expertise in hardware). In other cases, the problem requires an integrated software/hardware solution. The contractor uses a pre-established rate that applies to all troubleshooting performed by this department.

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

Recall that Cost Accounting Standard (CAS) CAS 418-50(a)(2)(ii)(B) says that an average cost or pre-established rate for labor may be used if the functions performed are materially disparate but the employees involved either all work in a single production unit yielding homogeneous outputs, or perform their respective functions as an integral team.

The contractor proposes using a pre-established rate of $40 per hour for each of the 40 workers. Some of the workers are painters, others are fabricators, and others are material inspectors. The end product of this group of workers is the assembly of the core unit for black boxes that are used in aircraft. Each of the core units produced is the same, i.e., they are homogeneous.

Homogeneous

Now let’s shine the spotlight on indirect cost pools. CAS 418 specifies that indirect cost pools must be homogeneous, and CAS 418 provides criteria you can use to determine if an indirect cost pool is homogeneous.

If each significant activity within the cost pool has the same or similar beneficial or causal relationship to the cost objectives as the other activities in the pool, then the pool is homogeneous.

One way to test an indirect cost pool to see if it is homogeneous is if the contractor were to allocate the costs separately, rather than from a single pool. If the end results are pretty much the same—if there is no material difference—when the costs are allocated separately or as part of the same pool, then this indicates that the

pool is homogeneous.

Homogeneous

Now let’s shine the spotlight on indirect cost pools. CAS 418 specifies that indirect cost pools must be homogeneous, and CAS 418 provides criteria you can use to determine if an indirect cost pool is homogeneous.

If each significant activity within the cost pool has the same or similar beneficial or causal relationship to the cost objectives as the other activities in the pool, then the pool is homogeneous.

One way to test an indirect cost pool to see if it is homogeneous is if the contractor were to allocate the costs separately, rather than from a single pool. If the end results are pretty much the same—if there is no material difference—when the costs are allocated separately or as part of the same pool, then this indicates that the

pool is homogeneous.

Example

For example, a contractor establishes a single manufacturing indirect cost pool that includes both assembly and fabrication functions.

The allocation base is total manufacturing labor. The assembly functions relate to assembly direct labor activities and the fabrication functions relate to fabrication direct labor activities.

Assuming there is a material difference in cost allocation if the costs were allocated separately, is this pool homogenous?

Give this some thought and then select the next tab to see the answer.

Example (cont.)

The pool is not homogeneous because the assembly functions have a causal/beneficial relationship only to assembly direct labor activities and the fabrication functions have a causal/beneficial relationship only to fabrication direct labor activities.

Thus, each activity in the pool does not have a similar beneficial or causal relationship to cost objectives as the other activities whose costs are also included in the pool, therefore, the pool is not homogeneous.

In this example, allocating overhead costs from the single pool will result in the contracts getting a disproportionate share of the overhead. Some contracts will get more than they should, while others will get less.

Inclusive

One final thing, CAS 418 goes on to say that, in addition to being homogeneous, the pool must include all indirect costs identified with the activity to which the pool relates.

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

A contractor establishes a single overhead pool that includes computer hardware and computer software support. The allocation base for the overhead pool is computer hours used.

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

Recall that Cost Accounting Standard (CAS) 418-50(b)(3) requires a homogeneous cost pool to include all the indirect costs identified with the activity to which the pool relates.

A contractor has an assembly overhead pool that includes the activities related to product assembly. The contractor includes indirect labor costs in the pool when indirect labor is performed by employees classified as “indirect workers.” However, the contractor charges indirect labor performed by employees that are classified as “direct workers” to the general overhead pool.

Bases

Now that you understand that indirect cost pools must be homogeneous and that they must include all the indirect costs associated with the activity in the pool let’s focus on appropriate allocation bases.

The allocation base must result in each cost objective receiving its fair share of the indirect cost that is being allocated.

Bases

Now that you understand that indirect cost pools must be homogeneous and that they must include all the indirect costs associated with the activity in the pool let’s focus on appropriate allocation bases.

The allocation base must result in each cost objective receiving its fair share of the indirect cost that is being allocated.

Requirement

Indirect cost pools that include a material amount of the cost of management or supervision of activities involving direct labor or direct material must be allocated on the basis of direct labor hours, direct labor dollars, or material dollars.

For example, if an indirect cost pool consists of the indirect costs of the assembly functions, then assembly direct labor hours or dollars may be an appropriate base.

And, CAS 418 also specifies that when the contractor is deciding whether to use a direct labor dollar or direct labor hour base, the base they select should be the one that, in the aggregate, is more likely to vary in proportion to the indirect costs being allocated.

[48 CFR 9904.418-50(d)(2)(i)]

Facility

This tab and the next two tabs present refinements to the basic requirement that was presented on the preceding tab.

If the indirect cost pool is comprised predominately of facility related costs, such as depreciation, maintenance, and utilities, then a machine-hour base is appropriate, such as fabrication machine hours.

[48 CFR 9904.418-50(d)(2)(ii)]

Indirect Cost Pool

Common Units

If there is a common production of comparable units, then a units-of-production base is appropriate, such as the number of navigation units produced.

[48 CFR 9904.418-50(d)(2)(iii)]

Indirect Cost Pool

Material

If the activity being managed or supervised is a material related activity (management of direct materials), then a material cost base is appropriate.

[48 CFR 9904.418-50(d)(2)(iv)]

Indirect Cost Pool

Summary Table

This table summarizes the CAS 418 requirements related to allocation bases for indirect cost pools.

Indirect Cost Pool With

Use this Allocation Base

CAS 418 Citation

A material amount of the cost of management or supervision involving direct labor or direct material

Direct labor hours. Direct labor dollars. Material dollars, unless 1, 2, or 3 apply

[48 CFR 9904.418-50(d)(2)(i)]

1. Facility related cost (e.g., depreciation, maintenance, and utilities)

Machine-hour base

[48 CFR 9904.418-50(d)(2)(ii)]

2. Common production of comparable units

Unit of production base

[48 CFR 9904.418-50(d)(2)(iii)]

3. Activity being managed or supervised is a material related activity

Material cost base

[48 CFR 9904.418-50(d)(2)(iv)]

Mentor Tips

The contractor is required to use one of the allocation bases, not all of them.

Audio Transcript

The contractor is required to use one of the allocation bases, not all of them.

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

A contractor has a manufacturing overhead pool. The pool includes supervision of the manufacturing department. The direct costs of the manufacturing department are comprised of assemblers, welders, riveters, fabricators, and painters.

The amount of supervision required for an hour of assembler work is the same as that required for an hour of welder, riveter, fabricator, or painter work. However, the welders are paid twice as much on average as the riveters. The riveters are paid twice as much as the assemblers, fabricators, and painters.

The contractor produces a variety of Government and commercial items. Some of the items require significant welding, while others require none. Also, some items may require fabrication and/or riveting, while others will not.

The contractor proposes using a direct labor dollars allocation base to allocate the supervision costs of the manufacturing department.

Base?

In the preceding question, you discovered how challenging it can be when you’re trying to decide whether a direct labor hour base or a direct labor dollar base should be used to allocate overhead costs.

Therefore, let’s take a look at another example where we have to decide between a direct labor hour or direct labor dollar allocation base.

Base?

In the preceding question, you discovered how challenging it can be when you’re trying to decide whether a direct labor hour base or a direct labor dollar base should be used to allocate overhead costs.

Therefore, let’s take a look at another example where we have to decide between a direct labor hour or direct labor dollar allocation base.

Example

In this example, the contractor has an engineering overhead pool for engineering supervision. The contractor has three levels of direct engineering labor: Level I, Level II, and Level III.

There are two contracts. The first contract has Level I engineers assigned to it, and the second contract has Level III engineers assigned to it. Typically, the Level I engineers require more supervision and they make a lower salary than the Level III engineers.

Now, if the contractor allocates engineering overhead on the basis of direct labor dollars, which contract will receive the greater engineering overhead cost allocation?

Give this some thought and then select the next tab to check your answer.

Answer

The contract that consists mainly of Level III engineers would receive a greater allocation of overhead costs if direct labor dollars are used as the allocation base. Recall that in accordance with CAS 418, the base should be used that is more likely to vary in proportion to the indirect costs being allocated.

In this case, the Level I engineers require more supervision than the Level III engineers; therefore a direct labor hours base is warranted rather than a direct labor dollars base.

Direct labor hours are more likely to vary in proportion to engineering supervision overhead costs than direct labor dollars, in this example.

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

A contractor has a machine overhead pool that is responsible for managing the employees that work on the company’s 100 fabrication machines and for maintaining the operation of those machines. There is a material amount of direct labor costs incurred by the employees that work on the fabrication machines.

The contractor groups all the costs of managing and maintaining the machines in a single homogeneous overhead pool. For the fiscal year, the costs of the machine overhead pool were comprised of the following.

Activity

FY Cost

Supervision and Management

$300,000

Depreciation (of fabrication machines)

$4,000,000

Supplies

$200,000

Utilities

$1,000,000

Indirect Labor (Other than Supervision and Management)

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

A contractor has a line overhead pool that accumulates the indirect costs associated with managing the production of garments. The assembly line has 75 employees that charge most of their time as direct labor, and also uses a large dollar amount of materials.

While the contractor produces many different types of garments, the basic manufacturing and production lines are predominately the same. About 90% of the production line is identical for all of the garments. The remaining 10% differs to allow for production of the unique qualities of the different garments.

An analysis shows that the difference in the production costs for the 10% is not material. Therefore, the line overhead pool is determined to be homogeneous, and the contractor includes all overhead costs associated with producing the garments in the line overhead pool.

The contractor selects the total number of garments produced as its allocation base (a units-of-production base).

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

A contractor has a material processing department. The nature of the contractor’s business requires that large amounts of material be delivered to various locations for use on contracts. When a contract requires a material delivery, a group of employees processes the order and delivers the materials. The cost of these employees is charged direct to the contract for which the materials will be used. The material processing pool includes the costs of supervising and managing these employees, as well as the cost of operating and maintaining the equipment (e.g., cranes and forklifts).

The contractor selects material cost as the allocation base.

Indirect cost pools that include material amounts of the cost of management or supervision of activities involving direct labor or direct material costs must be allocated to each of the following:

Final cost objectives

Goods produced for stock or product inventory

Independent research and development (IR&D) costs

Bid and proposal (B&P) costs

Cost centers used to accumulate costs identified with a process cost system (i.e., process cost centers)

Goods or services produced or acquired for other segments of the contractor and for other cost objectives of a business unit

Self-constructed, fabrication, betterment, improvement, or installation of tangible capital assets

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

Segment R has a machining department. The contractor has a machining overhead pool that includes only the indirect functions related to the activity of the machining department. The machining department does a significant amount of work for other segments of the company.

Requirement

So far, we have examined requirements related to indirect cost pools that include a material amount of the cost of management or supervision of activities involving direct labor or direct material.

But, what about those indirect cost pools that do not include a material amount of the cost of management or supervision of activities involving direct labor or direct material?

CAS 418 says that these pools must be allocated on the basis of resource consumption. And then CAS 418 specifies the allocation hierarchy in the next tab.

Requirement

So far, we have examined requirements related to indirect cost pools that include a material amount of the cost of management or supervision of activities involving direct labor or direct material.

But, what about those indirect cost pools that do not include a material amount of the cost of management or supervision of activities involving direct labor or direct material?

CAS 418 says that these pools must be allocated on the basis of resource consumption. And then CAS 418 specifies the allocation hierarchy in the next tab.

Hierarchy

Whenever possible, a measure of resource consumption must be used as the allocation base, if one is available and practical to ascertain.

If a measure of resource consumption is unavailable or impractical to ascertain, the output of the activities of the indirect cost pool must be used as the allocation base.

If neither resources consumed nor output of activities can be measured practically, a surrogate that varies in proportion to the services received must be used to measure the resources consumed.

[48 CFR 9904.418-50(e)(1), (2), and (3)]

Example 1

A contractor has an indirect cost pool that includes the cost of occupancy associated with the office building. The contractor needs a way to allocate this cost fairly among the final cost objectives that benefit from it.

In accordance with CAS 418, the contractor’s lead cost accountant first tries to find a resource consumption measure that would be practical to ascertain and use; however, she cannot identify one that applies in this situation.

Next, as CAS 418 mandates, she tries to find an output allocation base. After giving it some thought, she proposes using the number of square feet of space provided to the users as the output base. Her analysis reveals that this allocation base results in a reasonable, fair allocation of the occupancy costs among the final cost objectives that use the space. Under these circumstances, using square footage to allocate occupancy costs complies with CAS 418.

Example 2

A company has a corporate jet. Indirect costs associated with the jet are collected in a pool that does not include management or supervision costs of direct labor or direct material. Therefore, in accordance with CAS 418, the contractor needs to use a resource consumption allocation base to allocate the indirect costs of the corporate jet to the final cost objectives that use it.

The contractor tries to find a resource consumption measure that is reasonable and can be practically ascertained but cannot identify one. Therefore, the contractor decides to use the output measure of mileage as the allocation base.

Each final cost objective receives its share of the indirect costs in the pool based on the number of miles flown for that cost objective during the fiscal period. This practice complies with CAS 418.

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

A contractor operates a machine that uses a special brand of very expensive fuel to operate that the contractor buys in large quantities because the machine requires a substantial amount of the fuel to operate.

The machine provides a unique fabrication and weld for five unique Government and two unique commercial products. The machine requires about two hours of calibration before it can be used on a particular product. Thus, the machine is generally used for a minimum of eight hour increments on a particular product.

The contractor has an indirect cost pool that is comprised solely of the cost of the fuel. The contractor uses gallons of fuel expended as the allocation base for the pool.

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

Business Unit P has a facilities management department that manages the three buildings owned by the contractor. The costs of this department are accumulated in a facilities management pool. The pool is comprised of indirect labor, depreciation, utilities, and supplies.

The contractor is unable to ascertain the consumption of resources in relation to the use of the facilities by individual cost objectives. Therefore, the contractor selects an allocation base of square footage, which represents the output of the activities.

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

A contractor has a material handling overhead pool. The functions in the pool include the processing, inspection, and transfer of materials. The contractor is unable to ascertain the resources consumed or the output produced. Therefore, the contractor selects material cost as the allocation base.

Modified

CAS 418 includes requirements related to the contractor needing to modify or prorate the allocation base.

When the allocation base is the output of activities and the basic unit of output does not reflect the proportional consumption of resources, the output measure must be modified or more than one output measure used to reflect the resources consumed by the activity.

[48 CFR 9904.418-50(e)(2)(ii)]

Modified

CAS 418 includes requirements related to the contractor needing to modify or prorate the allocation base.

When the allocation base is the output of activities and the basic unit of output does not reflect the proportional consumption of resources, the output measure must be modified or more than one output measure used to reflect the resources consumed by the activity.

[48 CFR 9904.418-50(e)(2)(ii)]

Prorated

When the activities represented by an indirect cost pool provide services to two or more cost objectives simultaneously, the cost of such services shall be prorated between or among the cost objectives in reasonable proportion to the beneficial or causal relationship between the services and the cost objectives.

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

A contractor has a reproduction department. The department produces both color and black-and-white copies. The department also produces bound and unbound copies. The contractor selects an allocation base of number of pages produced. However, the number of pages produced is increased by 25% for color copies (the additional estimated cost of producing a color copy) and 10% for binding (the additional estimated cost of binding).

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

A contractor whose main office is located near Washington, D.C., maintains a corporate aircraft. The cost of aircraft is allocated to cost objectives on the basis of miles flown.

The contractor has numerous contracts, including Contracts E, F, and G. The managers of Contracts E, F, and G jointly attend a meeting in San Francisco via the corporate aircraft. The total roundtrip mileage is 4,500 miles. In determining the amount of miles in the allocation base for each cost objective, the contractor divides the mileage equally among the three managers, i.e., 1,500 miles goes to Contract E, 1,500 miles to the Contract F, and 1,500 miles to Contract G.

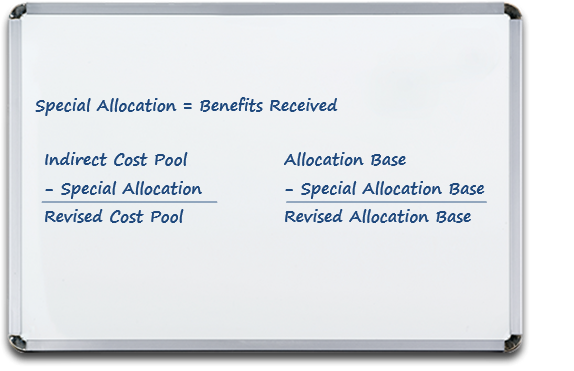

When a particular cost objective in relation to other cost objectives receives significantly more or less benefit from an indirect cost pool than would be reflected by the allocation of such costs using a base required by CAS 418, the Government and contractor may agree to a special allocation.

When the Government and contractor agree on a special allocation:

The amount of the special allocation must be commensurate with the benefits received.

The amount of the special allocation must be excluded from the indirect cost pool.

The data for the particular cost objective that is receiving the special allocation must be excluded from the base used to allocate the indirect cost pool.

[48 CFR 9904.418-50(f)]

Image DetailsImage shows a whiteboard. Written on it is 'Special Allocation = Benefits Received' below that are two different calculations. 'Indirect Cost Pool minus Special Allocation equals Revised Cost Pool' and 'Allocation Base minus Special Allocation Base equals Revised Allocation Base'

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

A contractor that normally assembles widgets at its plant enters into a contract (Contract Q) whereby the contractor supplies the labor, but the actual assembly will occur at the customer’s plant.

The assembly overhead pool includes the following functions:

Supervision

Utilities

Depreciation

Fringe Benefits

Supplies

The contractor requests a special allocation for Contract Q because of the unique nature of the contract. The contract does not incur facilities related costs such as depreciation and utilities. However, it does incur fringe benefits at the same rate as other contracts. It also incurs supervision and supplies, but at a lesser rate than the other contracts. The Government and contractor agree on a special allocation.

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

Segment T has an indirect cost pool that includes a number of functions, including occupancy costs. Segment T has thirty contracts. The segment requests a special allocation for eight of those contracts for the indirect cost pool. All eight contracts were awarded during the most recent fiscal year. The contractor contends that these eight contracts have a large number of workers in a small area of space, as compared to the other twenty-two contracts. Therefore, the contractor requests a special allocation for the eight contracts.

The following questions have been designed to reinforce key requirements of Cost Accounting Standard (CAS) 418 on direct and indirect cost allocations.

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

Select the icon for the Knowledge Check details, and then rely on those details as you answer the following questions.

Check your knowledge by answering the following multiple choice question.

Select the best answer and then select Submit.

As the preceding question confirmed, the next step is to calculate the differences that occur when multiple (separate) indirect cost pools are used instead of a single pool. The results of that calculation are as follows.

Segment Z Differences between Multiple and Single Indirect Cost Pools:

Let’s continue with the preceding challenge. Now, you need to compose your findings as to why the contractor’s practice does not comply with Cost Accounting Standard (CAS) 418. In your position statement, be sure to include if the single indirect cost pool is homogeneous and support your position with specific references and language from CAS 418. Once you have composed your position statement, and you are satisfied with your results, select “Reveal Answer” to compare your answer to one possible statement.

The contractor’s method does not comply with CAS 418. Each significant activity that is included in the cost pool does not have the same or similar beneficial or causal relationship to cost objectives as other activities whose costs are included in the cost pool [48 CFR 9904.418-40(b)].

Therefore, the pool is not homogeneous. Supervision relates to direct labor hours, indirect labor relates to direct labor dollars, occupancy relates to square footage, computer usage relates to the number of workstations or computer hours, and supplies relate to the number of employees.

In addition, the allocation of the costs of the activities in a single pool to each of the contracts results in a materially different allocation than would result if the cost of the activities were allocated separately [48 CFR 9904.418-50(b)(2)].

As shown in the analysis below, if the costs are allocated separately, using multiple pools, there is a significant difference in the allocation to contracts than there is if a single pool is used. Contract A receives $26,800 more ($126,800 - $100,000), Contract B receives $66,000 more ($466,000 - $400,000), Contract C receives $52,000 less ($228,000 - $280,000), and Contract D receives $40,800 less ($179,200 - $220,000).

That’s a lot of information! Let’s recap the main points before you proceed:

CAS 418 requires that business units must have a written policy for how they classify costs as direct or indirect.

CAS 418 also requires that the cost pools used to collect indirect expenses must be homogeneous. An indirect cost pool is homogeneous if:

Each activity in the pool has the same or similar beneficial or causal relationship to the cost objectives as all the other activities in the pool, and/or

There is no material difference when the costs are allocated from separate pools compared to when the costs are allocated from a single pool.

CAS 418 specifies that if there are significant costs of management or supervision in the indirect cost pool, then the contractor must use an allocation base that is representative of the activity being managed or supervised: direct labor hours, direct labor dollars, or material dollars, with these additional stipulations.

Pools with a material amount of facility related costs should use a machine-hour base.

Pools with common production of comparable units should use a unit of production base.

Pools with a material related activity should use a material cost base.

When there are no significant management or supervision costs, the indirect cost pool must be allocated over a resource consumption measure if one is available and can be practically identified; otherwise, a measure of output should be used. Or, if neither of those two can be used, then a surrogate that is representative of the resources consumed should be used.